- Market Context

- What Happened

- Why It Matters

- Sector Breakdown

- Risks to Watch

- What to Watch Next

- Final Outlook

Market Context

Growth investing on the TSX in 2026 has taken on a distinctly artificial-intelligence-inflected character that is reshaping how Canadian tech names are valued and followed. The same companies that led Canada’s post-pandemic equity recovery — Shopify most prominently — are now being re-rated not simply on the basis of revenue growth, but on whether their AI integration strategies are genuinely accelerating their competitive advantages. This is a subtle but consequential shift: investors are increasingly asking not just how fast a company is growing, but whether it is growing in the right direction to compound the benefits of AI-driven productivity over a multi-year horizon.

The backdrop for Canadian growth stocks entering June is more constructive than the technical recession headline would suggest. The TSX’s technology-adjacent names have demonstrated a capacity to draw institutional capital even as the broader index wrestles with macro uncertainty. The 2026 outlook includes optimism around nation-building initiatives — transit, energy security, and digital infrastructure — that could provide a durable multi-year tailwind for companies operating at the intersection of technology and Canadian economic development.

Valuations remain the central tension. Canada’s highest-growth names trade at premium multiples that require continued execution and the absence of guidance misses. In a recessionary environment, even a modest disappointment relative to elevated expectations can trigger a disproportionate repricing. Investors must weigh the opportunity against the valuation discipline required to participate in it responsibly.

Also Read: Best long term Canadian stocks

What Happened

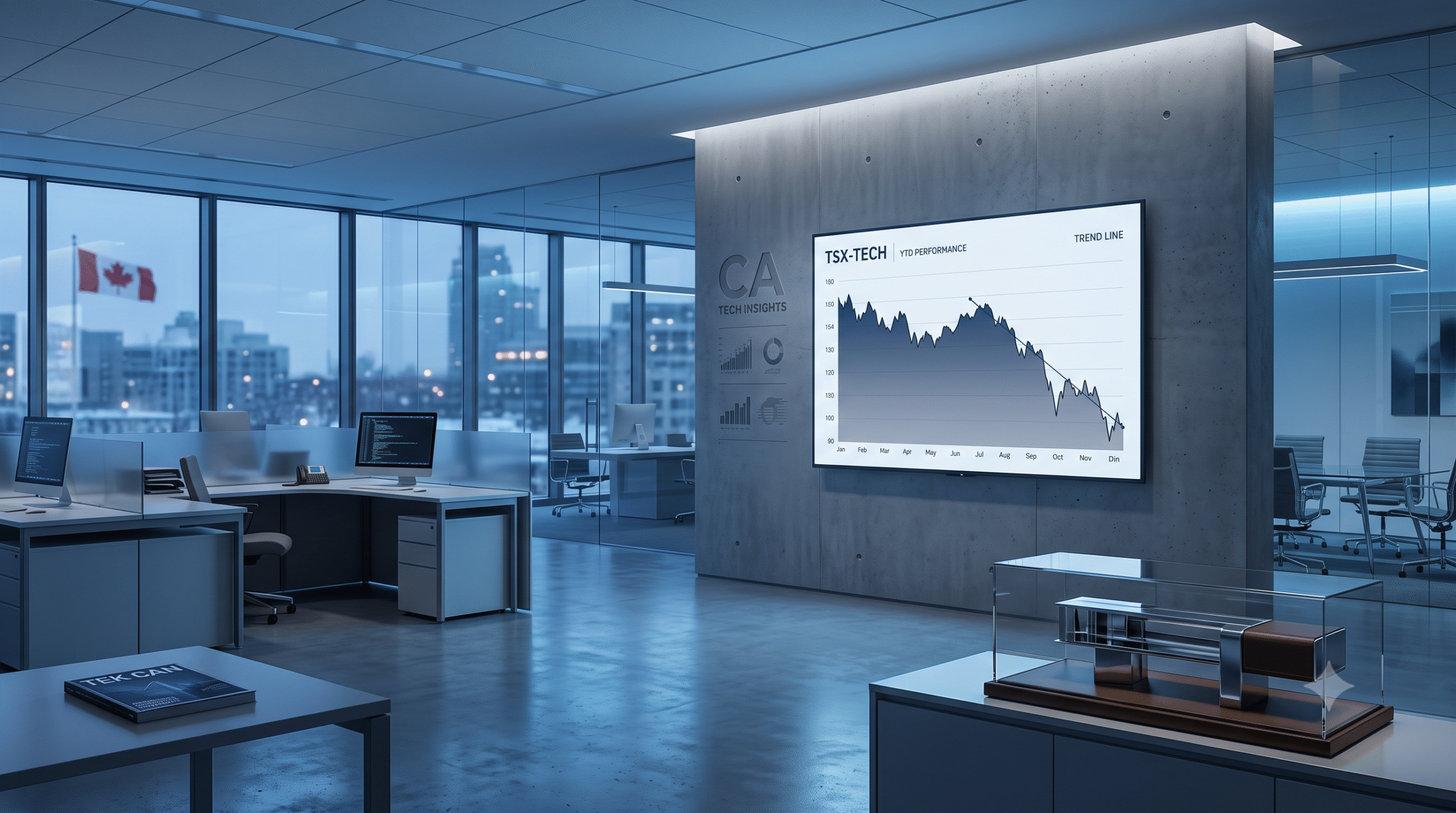

Shopify delivered the headline growth story of Q1 2026. Gross merchandise volume grew 35% and revenue expanded 34% year over year, with strong free cash flow and broad-based expansion across geographies and merchant segments. The company’s AI-driven tools, including its merchant assistant product and campaign optimisation features, are being credited with accelerating results, and new commerce protocol partnerships are strengthening its platform positioning. The quarter was a comprehensive beat that reinforced Shopify’s status as one of Canada’s most globally competitive technology assets.

In Monday’s TSX session, Shopify shares rose close to 2%, supported by AI optimism that followed a major semiconductor announcement from one of the world’s leading chip designers. The market is increasingly treating Shopify as a direct downstream beneficiary of the broader AI infrastructure buildout — not merely a commerce platform, but a technology company whose merchant tools are becoming meaningfully more powerful as AI models improve. Institutional investors, including at least one major growth-focused U.S. fund that disclosed a significant position in Q1, are treating Canadian tech as a legitimate AI-era investment.

Loblaw Companies tells a different growth story — digital transformation within a traditional retail framework. Its Q1 2026 earnings slightly exceeded analyst expectations, and the company’s investment in digital grocery and loyalty data capabilities is drawing investor attention beyond the conventional grocery-and-pharmacy narrative that defined Loblaw for decades.

Why It Matters

AI Is Becoming the Valuation Multiple Driver

The market’s willingness to pay a premium for AI-integrated growth businesses — even on the TSX, traditionally dominated by resource and financial sector weights — represents a structural shift in how the Canadian equity market is perceived and used by global institutional investors. Shopify is the most visible expression of this, but the broader implication is that Canadian technology names with credible AI integration stories may see their cost of equity capital improve over time as the investor base diversifies toward growth-seeking mandates.

Constellation Software — The Quiet Compounder

While Shopify captures the headlines, Constellation Software continues to compound shareholder wealth through one of the most disciplined capital allocation models on the entire TSX. As a serial acquirer of vertical market software businesses, the company benefits from recurring revenue streams and strong cash conversion, and its model of acquiring and improving niche software companies has generated exceptional long-term returns across multiple market cycles. In a volatile environment, that kind of predictable compounding carries a premium that may not be obvious from headline metrics alone.

Also Read: Safe investments for new investors

Sector Breakdown

The TSX growth landscape in June 2026 is usefully divided into three sub-categories: AI-native platforms, digital-transforming incumbents, and capital-efficient compounders. Shopify occupies the first category almost alone in Canada. Loblaw and Alimentation Couche-Tard represent the second — large incumbents deploying technology to improve economics and expand addressable markets. Constellation Software, and to some extent Canadian National Railway, represent the third: businesses that compound shareholder value through disciplined acquisition and reinvestment rather than dramatic revenue acceleration.

Alimentation Couche-Tard has transformed into a global convenience and fuel retail powerhouse through consistent same-store sales growth, strategic international acquisitions, and fuel margin management that has proven resilient across commodity cycles. Some analysts currently favour Couche-Tard over Loblaw as a long-term compounder, noting its superior valuation and stronger international growth optionality. Both names are worth understanding as distinct expressions of the Canadian consumer growth thesis.

National Bank is also drawing attention as investors assess its growth trajectory amid the current market environment. Analysts are closely watching whether the bank can maintain its momentum while navigating a technically recessionary domestic backdrop.

Also Read: Long term investing in Canada

Risks to Watch

Growth stocks carry the highest valuation risk in any slowdown scenario, and the TSX’s premium-multiple technology names are no exception. If Q2 GDP data shows the recovery from Q1 is weaker than preliminary estimates suggested, high-multiple names would face simultaneous earnings-estimate cuts and multiple compression — a doubly painful outcome for investors holding at current valuations. Shopify’s international revenue growth creates meaningful foreign exchange exposure and concentration risk in the U.S. market, a vulnerability that becomes more pronounced as the USMCA review approaches July 1. Guidance misses can be particularly brutal for growth names: the market expects excellence, and anything short of it tends to be repriced swiftly and without mercy. Position sizing discipline is not optional in this segment.

What to Watch Next

Shopify’s next earnings release will be the critical near-term data point for TSX technology growth investors. Any guidance update — particularly on free cash flow margins and the monetisation trajectory of AI-enabled merchant tools — will set the tone for the stock through the summer and into Q3. Constellation Software’s next acquisition announcement, whenever it arrives, will be read as a signal of how the company views private market valuations for vertical software assets. For broader growth sentiment, the Bank of Canada’s June 10 decision matters: a hold with neutral language removes one of the few remaining macro headwinds for premium-multiple growth stocks, at least temporarily.

Final Outlook

TSX growth stocks in June 2026 are performing above expectations given the macro backdrop. The AI-driven re-rating of names like Shopify has provided a thematic catalyst that has partially insulated the growth segment from the drag of the technical recession narrative. Constellation Software and Couche-Tard continue to demonstrate that disciplined capital allocation — not just revenue acceleration — is a durable and repeatable source of TSX growth outperformance across market cycles.

Investors should approach the category with a clear distinction between companies where growth is validated by improving cash flow and those where growth is aspirational and dependent on a future profitability inflection that has yet to arrive. That distinction has never mattered more than it does in an environment where the recession label is freshly applied and investor patience is finite.

Sign Up For our Newsletters to get latest updates