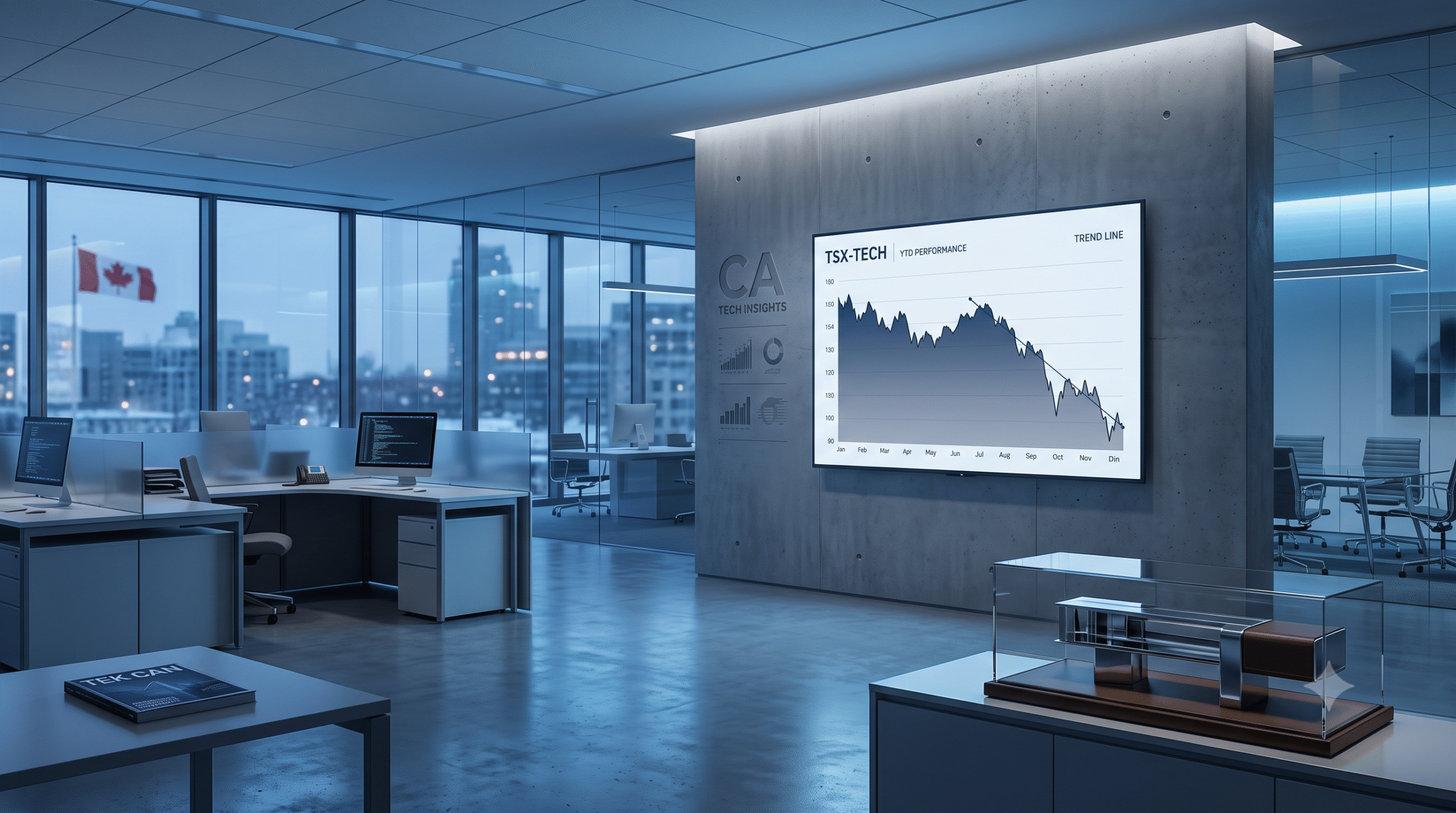

Shares of Docebo (TSX: DCBO) are trading near $23.81, down approximately 46% over the past year, yet the company’s fundamental picture continues to challenge the bearish narrative. The Toronto-based AI-powered learning management platform delivered a 29% earnings surprise in its most recent quarter — posting $0.61 EPS against a $0.48 consensus estimate — while revenue came in at $85.97 million, essentially in line with expectations. Multiple analysts have maintained or upgraded their outlook, with ATB Cormark raising its target to $36 from $35 and CIBC holding an Outperform rating with a $38 target. The consensus analyst price target of approximately $40.71 implies upside of over 70% from current levels.

The disconnect between Docebo’s stock performance and its underlying business can be traced to sector-wide selling in Canadian growth and tech stocks, combined with investor concern that generative AI could disrupt the learning management space rather than enhance it. Docebo has leaned into that narrative by positioning its platform as an AI-native solution — integrating AI authoring tools, skills intelligence, and automated content delivery to enterprise clients. With 94% of revenue coming from subscriptions, the business carries predictable recurring cash flow and minimal customer churn risk. The e-learning services industry is projected to grow at roughly 19% annually through 2030, providing a significant structural tailwind.

Also Read: Top Canadian tech AI stocks

For TSX growth investors, the key tension is valuation versus competitive positioning. Docebo trades at a price-to-earnings ratio near 10–12x trailing earnings — inexpensive for a software business with positive free cash flow and double-digit EPS growth. However, critics argue the company lacks the competitive moat of larger enterprise software players, and that its market remains crowded with better-capitalized rivals. Scotiabank has lowered its broader tech targets, but CGI Inc. and Docebo have seen divergent analyst treatment, with Docebo retaining more buy-side support.

Also Read: Long term investing in Canada

The immediate catalyst to watch is the Q1 2026 earnings report scheduled for May 8. Investors will focus on annual recurring revenue growth, net revenue retention, and management’s commentary on AI competition and enterprise sales pipeline. If Docebo can demonstrate consistent margin expansion alongside revenue growth, it may finally bridge the gap between its fundamental performance and a stock price that currently prices in a far more pessimistic outcome.

Sign Up For our Newsletters to get latest updates