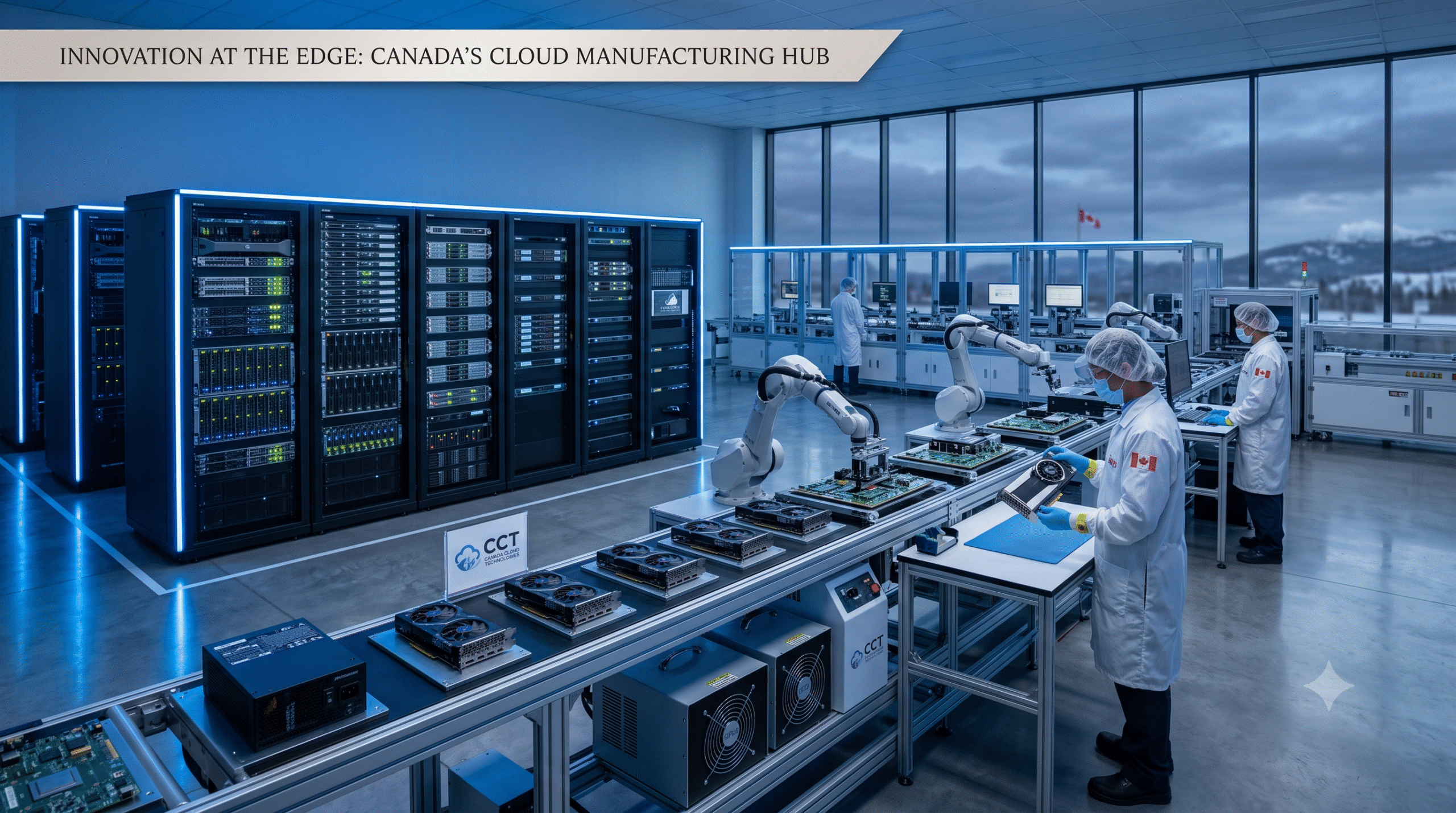

Celestica reported December quarter revenue of $3.7 billion, up 44% year-over-year, driven by explosive demand for AI infrastructure from hyperscale cloud providers. Adjusted earnings jumped nearly 70% to $1.89 per share as the Toronto-based hardware manufacturer capitalized on its market-leading position in high-bandwidth networking equipment.

The company now commands 41% market share across 200-gigabit, 400-gigabit, and 800-gigabit Ethernet switches, with production already ramping for 1.6-terabit platforms and investment underway for 3.2-terabit technology. This dominant position in next-generation networking hardware positions Celestica at the center of the AI buildout, as cloud providers upgrade infrastructure to support large language models and data-intensive workloads. Management expects this momentum to continue through 2028 as data center capital expenditures approach $1 trillion.

Also Read: Dividend paying stocks Canada

Celestica’s stock has more than tripled in the past year, trading near $404 with a market capitalization exceeding $46 billion. The company has transformed from a contract manufacturer into a critical supplier for Google, Meta, and Amazon’s custom silicon projects. Unlike software companies facing AI disruption concerns, Celestica benefits directly from the physical infrastructure requirements of artificial intelligence deployment.

Also Read: Best long term Canadian stocks

For 2026, management projects revenue reaching $16 billion with operating margins of 7.8% and earnings of $8.20 per share. The company plans to invest approximately $1 billion in capital expenditures to expand manufacturing capacity in Texas and Thailand. Analysts tracking the stock forecast earnings growth from $3.88 in 2024 to $11.81 by 2027, reflecting confidence in sustained AI infrastructure spending even as the technology matures from training to inference workloads.

Sign Up For our Newsletters to get latest updates