Unlock Premium Articles for Exclusive Insights!

You are reading a free article. Enter your details to unlock full access.

By submitting your details to unlock full access.

What Happened

The May 1 session produced several notable earnings outcomes. Fairfax Financial slumped 7.5% after missing its earnings estimate. Magna fell 5% on disappointing order figures. TC Energy and Agnico Eagle Mines each fell over 1% following their quarterly reports. Imperial Oil sank 4% after its earnings release. Air Canada abandoned its 2026 guidance, sending its shares lower.

That string of misses and guidance withdrawals represents a meaningful shift in tone from the relative optimism of earlier in the year. The domestic GDP report released in late April, which highlighted subdued consumer spending, compounded the negative sentiment in financial and consumer-facing sectors.

The TSX rose approximately 35.95% compared to the same time last year, a reminder that despite the near-term noise, the medium-term trend for Canadian equities has been strongly positive. Whether that trend can continue into the second half of 2026 depends significantly on how the geopolitical and monetary policy picture evolves.

Why It Matters

Earnings Misses Reflect Macro Pressures

The breadth of Q1 earnings disappointments — spanning financials, industrials, auto parts, integrated energy, and transportation — suggests that the macro headwinds are not contained to a single sector. Rising input costs, cautious consumer behaviour, and the disruptive effects of the Iran conflict on supply chains are showing up broadly in corporate results. Investors should watch whether the Q2 earnings season, which begins in earnest in July, reveals a similar pattern or whether conditions stabilise.

Mark Carney’s Pipeline Signal

Prime Minister Mark Carney indicated in late April that a new oil pipeline out of Alberta will likely be built. That signal, combined with the Canada Strong Fund announcement, suggests a government that is increasingly focused on resource export infrastructure — a medium-term positive for Alberta producers and pipeline operators if regulatory approvals proceed.

Sector Breakdown

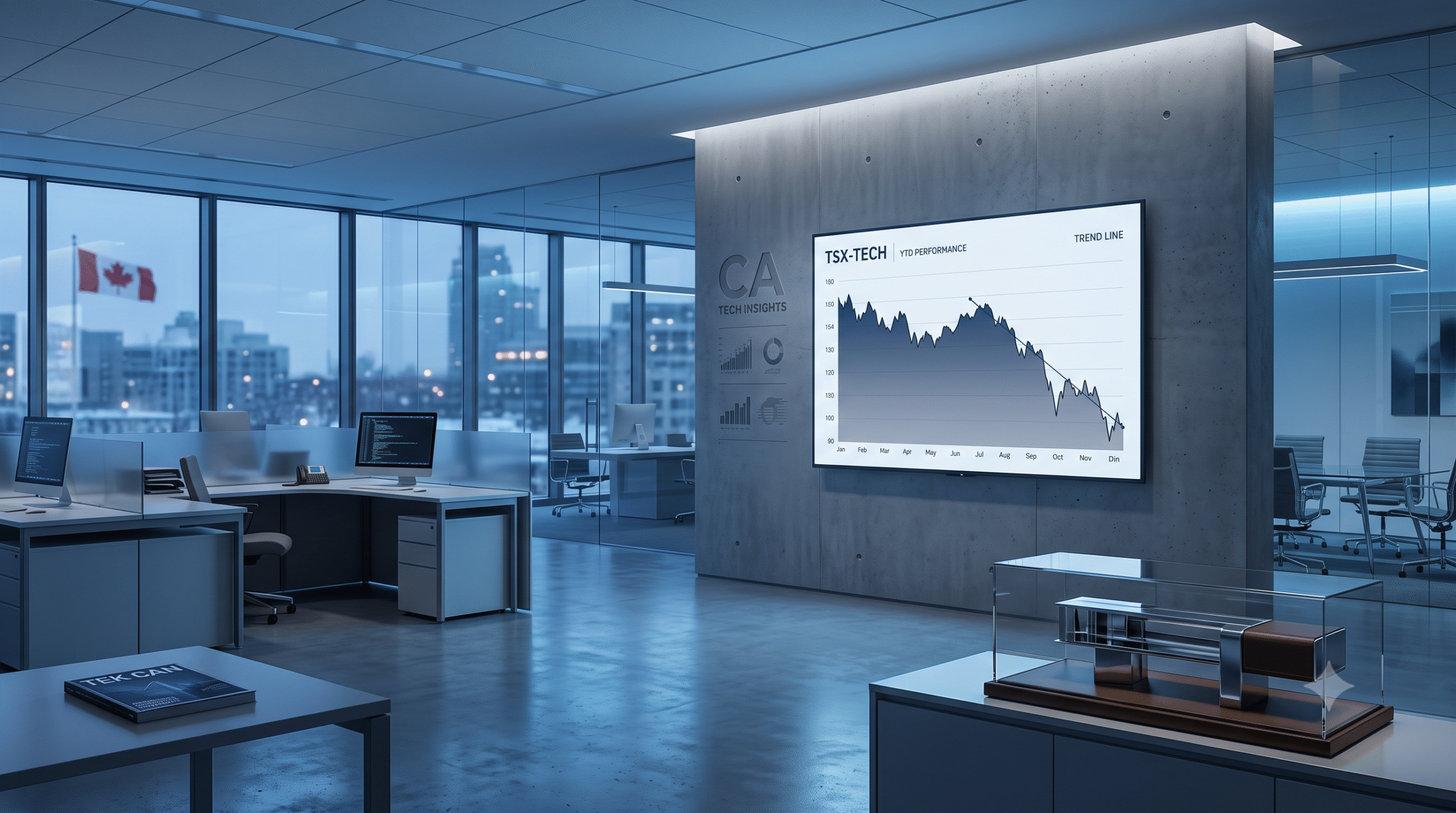

Financial services — the TSX’s largest sector weighting — has been the most important story for investors this earnings season. The combination of slower loan growth, rising credit concerns, and the potential for higher rates creates a complex picture for banks that were until recently benefiting from a rate-cut cycle. Energy, despite record-high commodity prices, has faced selling pressure as OPEC+ supply increases and cost inflation create valuation uncertainty. Technology has been a relative outperformer, with AI-related names attracting capital even as valuations remain stretched.

As of early May 2026, approximately 99 companies on the S&P/TSX Composite Index are reporting earnings, and the results so far have been more mixed than investors had anticipated entering the season.

Risks to Watch

The Canadian 5-year bond yield is at 3.1%, with ongoing bond market volatility expected in a tight range as uncertainty over the June US trade review and Iran conflict persists. For equity investors, rising bond yields reduce the relative attractiveness of stocks, particularly those trading at elevated multiples. The US-CUSMA trade review this summer represents a genuine binary risk: a favourable outcome would remove a major overhang, while adverse terms could trigger renewed selling in export-oriented Canadian companies.

Also Read: Best long term Canadian stocks

What to Watch Next

The calendar for Canadian investors is dense with catalysts over the coming six weeks. The Bank of Canada rate decision on June 10 is the single most important domestic event. The US-CUSMA trade review — with unknown timing but expected this summer — is the most significant macro risk. Ongoing monitoring of Strait of Hormuz developments and oil price movements will also be critical. Finally, the TMX Group, which reported Q1 2026 results on May 4, provides useful insight into trading volumes and capital markets health that can help investors gauge broader market sentiment.

Also Read: Safe investments for new investors

Final Outlook

The TSX has held up remarkably well given the scale of the macro challenges it faces. A year-over-year gain of approximately 36% reflects the real return of the commodity supercycle combined with strong financial sector performance, even as more recent sessions have been choppy. For investors managing diversified Canadian equity portfolios, the near-term environment calls for a defensive bias within risk positions — favouring companies with pricing power, strong balance sheets, and low leverage — while maintaining long-term exposure to Canada’s structural strengths in energy, resources, and financial services.

Sign Up For our Newsletters to get latest updates