- Market Context

- What Happened

- Why It Matters

- Sector Breakdown

- Risks to Watch

- What to Watch Next

- Final Outlook

Market Context

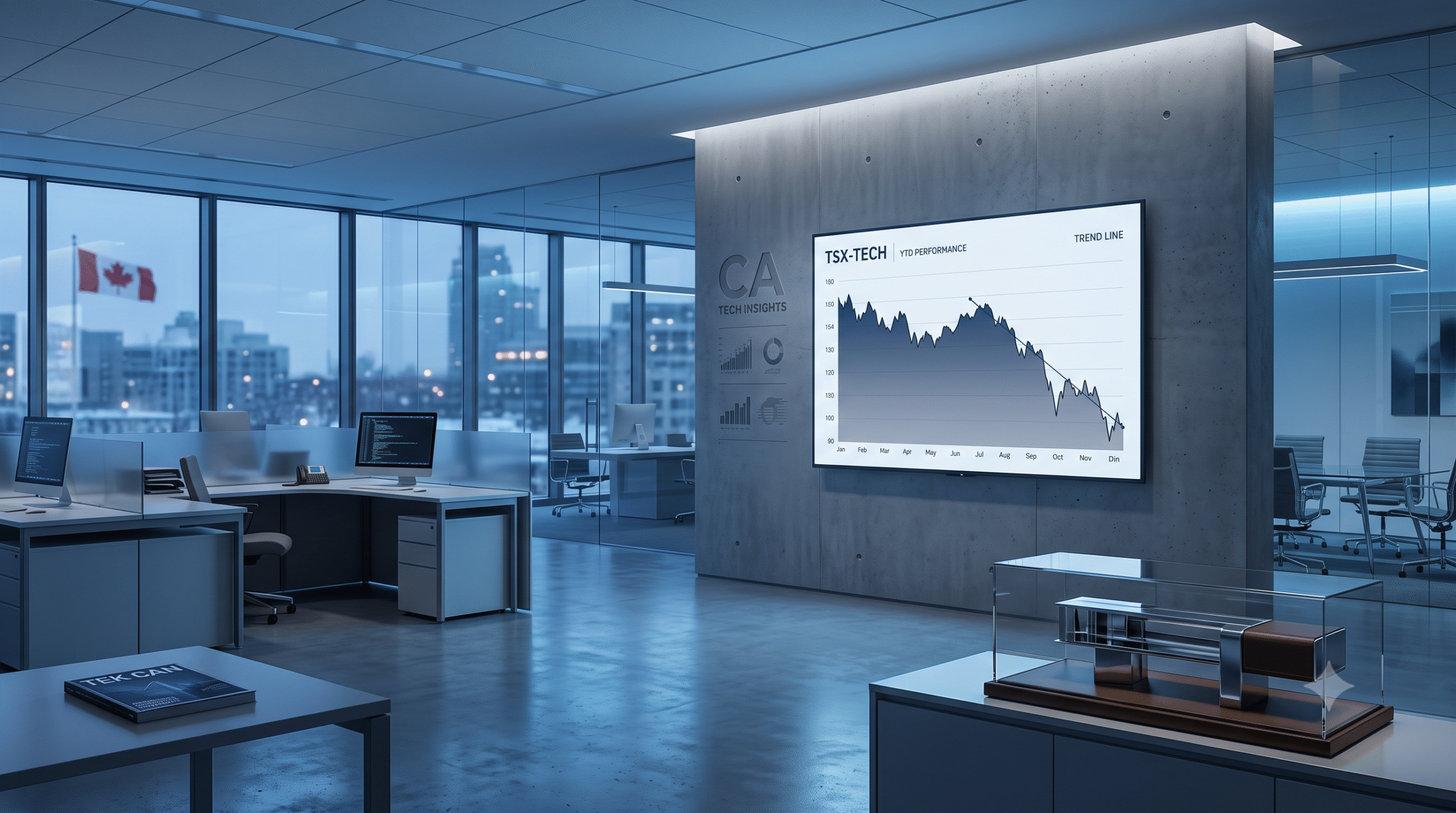

Growth investing on the TSX entered an uncomfortable moment of truth over the final days of the week ending June 5. The collapse in AI-hardware sentiment triggered by Broadcom’s demand update — and amplified by a broader risk-off selloff driven by a hot employment print pushing bond yields higher — produced a sharp, broad repricing of premium-multiple technology names. The Nasdaq’s 4.18% Friday decline was its worst since April 2025, and it carried Canadian tech names down with it regardless of company-specific merit. Shopify fell 5.4% and Celestica plunged 12.3%, each for different but related reasons, and the TSX technology segment as a whole gave back a meaningful portion of its recent gains in a single session.

The critical question for growth investors entering June 8 is whether last Friday’s selloff represents a temporary sentiment dislocation — the kind of event that resolves over weeks as fundamental earnings quality reasserts itself — or whether it is the opening move in a more sustained repricing of AI-related growth stocks as the underlying demand narrative becomes more contested. The answer likely differs meaningfully between companies, and that distinction is precisely the analytical challenge that defines growth investing in volatile markets.

The broader context is also worth holding carefully. The TSX is up more than 31% over the past year. Celestica, even after its Friday decline, has generated a five-year total shareholder return of approximately 1,729% — an extraordinary compound. Shopify has delivered consistent 30%+ revenue growth for multiple consecutive quarters and authorised a CA$3 billion share repurchase just days before Friday’s selloff. These are not structurally impaired businesses; they are businesses experiencing the valuation volatility that comes with high expectations and macro-driven discount rate pressure.

Also Read: Long term investing in Canada

What Happened

Celestica’s 12.3% Friday decline — following an 8% drop Thursday — came in the immediate aftermath of Broadcom’s earnings update. The catalyst was specific: Broadcom’s revenue share with Alphabet for tensor processing units is expected to fall from approximately 95% in 2026 to 80% in 2027 and 65% in 2028 as the Taiwanese semiconductor company MediaTek gains share. For Celestica, which has become one of the most important AI hardware suppliers — assembling and manufacturing components for the large-scale data centre buildout — the implication is that its own customer relationships with hyperscalers may similarly face competitive pressure over time. Celestica had hit a 52-week high of approximately CA$474 on June 2, just two days before the cascade began, and the speed of the reversal from record high to double-digit selloff within three sessions is a pattern associated with valuation resets after extended momentum runs.

It is important to note what did not change: Celestica’s Q1 2026 results, reported in April, showed revenue of US$4.05 billion — up 53% year over year — with strong adjusted earnings per share. The company raised its full-year 2026 guidance to US$19.0 billion in revenue and US$10.15 in adjusted EPS. A manufacturing expansion at Fort Worth, Texas is expected to bring over 1,700 new full-time roles. None of that changed in the past week. What changed is the market’s willingness to pay the forward multiple that was embedded in the CA$474 price point, once the AI chip supply concentration risk became more salient.

Shopify’s 5.4% decline was driven more by macro factors — bond yield pressure, sector risk-off, and the chip-adjacent AI sentiment washout — than by anything Shopify-specific. The company had authorised a CA$3 billion buyback programme earlier in the week and has posted 34% revenue growth in Q1 2026. Its fundamentals have not changed. The selloff is a macro overlay on a solid underlying business.

Why It Matters

Celestica’s Valuation Reset Separates Hardware from Platform

Celestica is fundamentally a hardware manufacturer — it assembles physical components for data centres. The competitive risk identified in Broadcom’s update — hyperscalers diversifying their supply chains — is a risk that applies equally to hardware assemblers who supply those hyperscalers. If the hyperscalers are reducing concentration risk with their chip designers, they may pursue the same logic with their hardware assemblers over time. That structural question is new and is now legitimately embedded in the investment thesis. Celestica’s long-term earnings trajectory may be unaffected, but the risk premium applied to that trajectory has expanded.

Also Read: Stock investment Canada for beginners

Software Platforms Are More Insulated

Shopify’s decline is essentially collateral damage from a hardware-specific concern. Commerce platforms, vertical market software businesses like Constellation Software, and logistics technology names face none of the supply-concentration risks that drove the Broadcom-to-Celestica contagion. If anything, the repricing of hardware names makes the comparative case for cash-generative software platforms stronger. Constellation Software’s 170% net income growth in Q1, its recurring revenue model, and its complete insulation from hardware supply chain dynamics make it a natural beneficiary of any investor rotation away from premium hardware names.

Sector Breakdown

The TSX growth landscape entering June 8 is more segmented than it appeared a week ago. Constellation Software and Topicus.com — both trading below estimated fair values based on discounted cash flow analysis — sit in the compounder category that has proven most resilient through previous tech selloffs. Shopify occupies a middle position: an AI-integrated platform with genuine growth and a management team confident enough to buy back stock at current prices, but vulnerable to broad risk-off selloffs that affect premium-multiple names without regard to underlying quality. Celestica is in a recalibration phase where the market is repricing its long-term growth trajectory against a more competitive hardware supply chain backdrop. And earlier-stage names like Lightspeed Commerce and Electrovaya remain the highest-risk, highest-potential subgroup within the growth universe.

Risks to Watch

The Bank of Canada’s June 10 statement carries direct multiple-compression risk for growth names. Higher discount rates from any hawkish tilt mechanically reduce the present value of future growth earnings, and high-multiple stocks bear the brunt of that compression. Celestica’s hyperscaler customer concentration risk has been freshly identified and will remain in focus until company management addresses it in a formal update. Shopify’s USMCA exposure — the majority of its merchant base operates in or through the U.S. market — means the July 1 trade review carries direct revenue geography risk. For Constellation Software, the primary risk is acquisition cost inflation if private market valuations for vertical software businesses remain elevated, which could slow the pace of value-accretive acquisitions that underpin the compounding model.

Also Read: Safe investments for new investors

What to Watch Next

Celestica’s next management update — whether in formal earnings guidance or a conference appearance — will be closely scrutinised for any commentary on hyperscaler customer diversification trends and what that means for their assembly volume outlook. Shopify’s Q2 earnings report will be the most watched single corporate event for TSX growth investors this summer. Any formal guidance update on free cash flow margins and the financial services expansion regulatory application will be critical inputs for the stock’s multiple post-selloff. Constellation Software’s next acquisition announcement is always a catalyst — it signals whether the company is finding private market valuations investable in the current environment. Bank of Canada language on June 10 sets the discount rate context for all of the above.

Final Outlook

TSX growth stocks on June 8 are navigating the combination of a technology sentiment reset — driven by Broadcom’s AI chip demand update — and a macro backdrop that is moving against premium multiples through rising bond yields. The session-level damage is real. Celestica’s 12.3% Friday decline and Shopify’s 5.4% loss require a thoughtful response rather than a reflexive one. The analytical distinction that matters most is between companies where the selloff has changed the fundamental thesis and companies where it has merely changed the near-term price.

For Constellation Software and Shopify, the evidence continues to support the fundamental thesis — Q1 earnings were strong, buybacks are active, and the businesses are not directly affected by hardware supply concentration risk. For Celestica, the thesis has been modestly complicated by an emerging structural question about hyperscaler supply diversification, and that question will take time and additional data to answer. Investors with longer time horizons may find the current dislocation in quality names to be an opportunity; those with shorter horizons should be cautious about catching a falling knife in the midst of a macro-driven selloff week.

Sign Up For our Newsletters to get latest updates